TL;DR: The 60-Second Guide to Salon Coverage

Here’s a primer on the what and why of salon insurance:

- Salon insurance is designed to cover third-party injuries and property damage claims that are caused by or happen at your business (and it can protect against other risks, too)

- Salon insurance is meant for salon owners with multiple stations and employees, while booth renters insurance is for independent stylists who rent a chair or station

- Beauty & Bodywork Insurance (BBI)’s salon insurance includes two essential coverages: general liability, for general client accidents at your salon, and professional liability, for injury claims related to you or your stylists’ services

- Popular salon insurance add-ons include tools and supplies (inland marine), cyber liability, workers compensation, and sexual abuse and molestation (SAM) coverage

- A certificate of insurance (COI) serves as proof of your active coverage and may also list additional insureds, such as your landlord, showing that your liability coverage extends to them

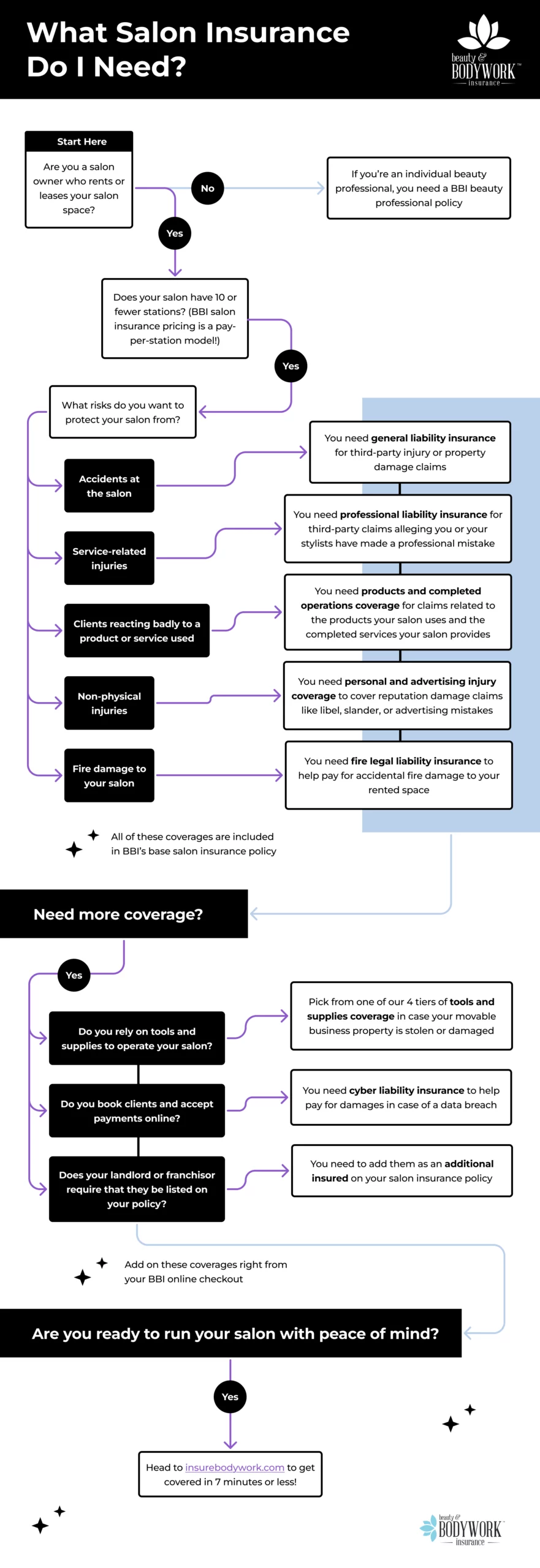

What Insurance Do I Need Based on How I Work?

Salon owners who run a physical salon in a leased space, with multiple stations and stylists on payroll, need salon insurance (also known as salon owners insurance).

Cosmetologists who work as independent contractors, rent a booth or station, or offer mobile services need a solo beauty professional policy, such as a cosmetologist insurance or hair stylist insurance policy.

Choosing the Right Insurance 101

➡️If you’re responsible for salon employees, you typically need salon insurance

➡️If you work solo, you typically need an individual policy, such as booth renters or cosmetologist insurance

The key difference: A salon policy covers the business + all stations, while an individual policy covers just you and your services.

Use this flowchart to find the right coverage for your beauty business in just a few steps.

What Coverage Do I Need if I Own a Salon?

If you own a salon, you need salon insurance to help protect your business from liability claims, especially if you:

- Operate in a rented or leased space

- Have up to 10 stations, chairs, or booths

- Need blanket coverage for all working stylists

Most lease agreements require proof of general liability insurance with set minimum limits (for example, a $3 million aggregate limit). BBI’s salon owner policy combines general and professional liability so you can easily meet insurance requirements and safeguard your salon from common industry claims.

BBI’s salon insurance uses a pay-per-station model, so your premium is based on the number of stations you want to cover. A single policy covers all your stations and any stylists who work them, automatically.

Salon owners often add optional coverage to enhance their protection, such as:

- Tools and supplies (inland marine) coverage for their movable business property

- Cyber liability coverage to help with data breach response and recovery

- Workers compensation insurance (typically legally required if you have employees) to help cover work-related injuries

➡️If your landlord says you need insurance to meet the lease contract, verify the type of coverage (typically general liability) and limits required, then match those to a salon insurance policy.

Explore more: Guide to Salon Liability Insurance.

What Coverage Do I Need if I Am a Booth or Chair Renter?

Booth renters need individual coverage through a booth renters insurance policy. Like salon insurance, this coverage protects against common third-party liability claims, except it’s designed for solo practitioners who rent a booth, chair, or station.

Salons typically require booth renters to carry their own liability policy. For example, the business owner may ask for the following before allowing you to work in their space:

- General liability insurance

- Minimum coverage limits (such as a $3 million aggregate limit)

- Proof of coverage via a certificate of insurance (COI)

- Their salon listed as an additional insured

If you rent a booth at a salon, the salon’s insurance policy typically does not cover you, which is why it’s a common industry practice for salons to require individual contractors to have their own coverage.

➡️If a salon owner says you need insurance before you can rent a booth, verify the requirements, including coverage type and limits, before purchasing your policy.

What Coverage Do I Need if I’m an Independent Stylist or Work at Multiple Locations?

Independent stylists who work at multiple salons or offer mobile services need hair stylist insurance. This coverage helps you meet insurance requirements at multiple locations and follows you wherever you work — all under a single policy.

While salon insurance is designed to cover a salon business (for example, a salon owner and all stations, plus their stylists), hair stylist insurance is tailored for the individual stylist who works at a salon as an independent contractor, or at events, clients’ homes, or their own home studio.

To work at a salon, you typically need:

- General liability insurance

- Minimum coverage limits (such as a $3 million aggregate limit)

- Proof of coverage via a certificate of insurance (COI)

- The salon listed as an additional insured

Hair stylist insurance, cosmetologist insurance, and booth renter insurance are all the same coverage with different names. For BBI’s affordable beauty professional insurance cost, get combined general and professional liability (with options for coverage add-ons) and meet the above requirements effortlessly.

➡️If you’re working at multiple locations or events, check each location’s insurance requirements in advance so your policy meets all of them.

Are you a My Salon Suite member? Get coverage recommended by My Salon Suite itself: Coverage for My Salon Suite Professionals.

What Do I Need to Know About Proof of Insurance?

Certificate of Insurance 101

What it is: Proof of coverage

Used for: Leases, salon agreements, event requirements

Turnaround time: Instant with BBI

Common mistakes: Incorrect names or missing wording

What Is a COI and How Do I Get One?

A certificate of insurance (COI) is a document that proves your coverage is active and meets certain requirements. You’ll need it if a person or business specifically asks for it to verify your coverage.

After purchasing BBI salon insurance, you get instant access to your certificate of insurance through your user dashboard. Download your copy, then email or upload it so the requester can double-check that your insurance is all set.

➡️ If a landlord asks for a COI, request their exact requirements first, then download your COI and verify all details match before sending.

Why Does My Salon, Landlord, or Venue Need Proof I Have Insurance?

Businesses need proof that you have active insurance because it confirms you’ve transferred your liability risk to an insurer, making it “safer” to work with you. Salon owners, landlords, or venues often ask to be listed as an additional insured for protection in case they get pulled into a claim related to your work.

These qualified third parties may have set rules on how much coverage you must carry (coverage limits) or other special wording as a way to manage their own risk when entering contract agreements with you.

What Info Do I Need to Request a COI Correctly?

Confidently handle COI requests by asking the landlord or venue to confirm:

✔️ Limit requirements

✔️ Business address

✔️ Certificate holder wording

✔️ Additional insured wording

✔️ Any additional endorsement wording

✔️ Deadline for COI submission

On your end, ensure you have the correct:

✔️ Business name and entity type

✔️ Policy active dates

✔️ Location covered

✔️ Services covered

After confirming all the details on your digital COI, download and submit it. With BBI, you don’t need to request and wait for your COI — it’s always ready to go right from your user dashboard.

Additional Insureds 101

What it is: Extension of coverage to qualified third parties

Used for: Adding landlords or property managers to your policy

How to add: During checkout or afterward through your dashboard

Common mistakes: Incorrect names, addresses, or details

How Do I Add My Salon or Landlord as an Additional Insured?

Easily add your salon or landlord as an additional insured during the BBI checkout process or any time afterward through your user dashboard — it only takes a few minutes!

Once you add the party as an additional insured on your policy, your liability coverage extends to them in case they’re named in a claim related to your work. It’s a smart way to reduce risk for both of you, but remember coverage (what’s included and what’s not) is still defined by your original policy terms.

Always ensure you have the correct business name, address, and contact information for additional insureds. Otherwise, you’ll need to redo the endorsement so it reflects the right details.

Quick Explainer: Requests for certificates of insurance and additional insureds are common for both salon owners and independent stylists. Salon owners usually receive these from their lessors, such as a landlord, while independent stylists are often asked by locations or events where they provide services, like salon owners and event organizers.

What Does Salon Insurance Cover?

| Example Scenario | The Coverage That Can Help |

|---|---|

|

A client slips on a wet floor and gets injured |

|

|

A client claims your salon’s color service caused a scalp injury |

|

|

A faulty hot tool causes a fire, which damages your leased space |

|

|

A competitor claims you stole their branding and sues your business |

|

|

A client alleges the products your stylist used caused a severe allergic reaction

|

|

|

A client’s family member needs quick medical care after getting nicked on a pair of scissors |

|

|

Your tools or equipment are stolen while in transit |

Tools and supplies coverage (optional) |

|

A data breach exposes clients’ credit card details |

Cyber liability insurance (optional) |

|

A client accuses a staff member of sexual misconduct |

Sexual abuse and molestation (SAM) coverage (optional) |

|

An employee gets injured while working at your salon |

Workers compensation insurance (optional) |

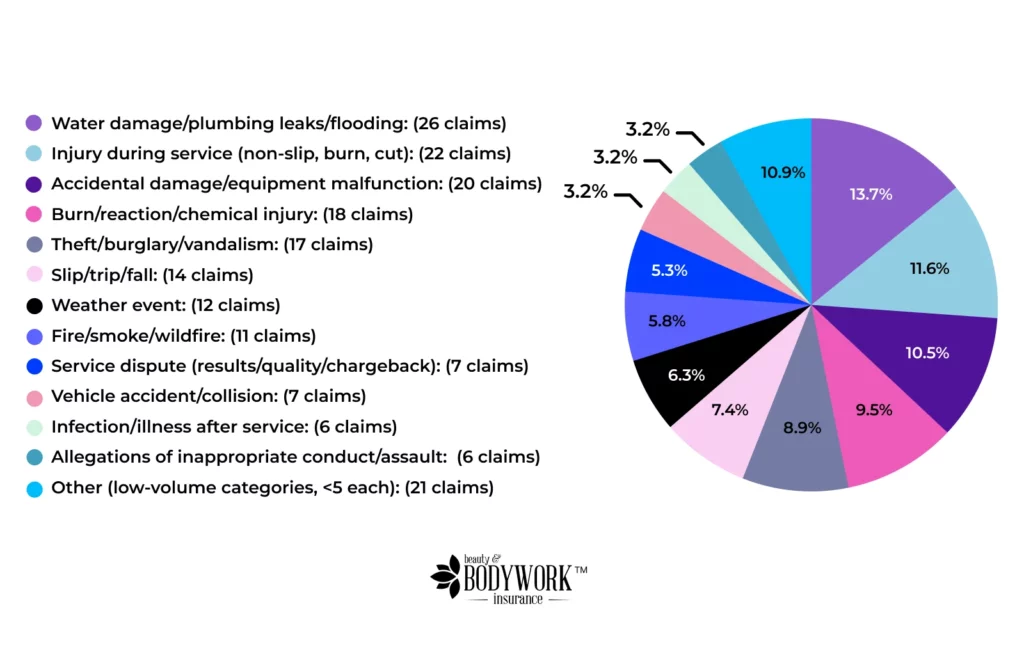

A Real-Life Insurance Claim

In 2025, BBI’s biggest claim incurred was a fire loss at a Florida spa. The blaze started on the property and destroyed the business’s personal property. The cost? $261.792 to help get the business back up and running.

According to our Insurance Statistics 2025 Lookback Report, these are some of the most common claims filed by your peers:

- Water damage

- Injury during service

- Equipment malfunction

- Chemical burns and allergic reactions

- Theft of business property

- Slip-and-fall injuries

Top BBI Claims by Frequency in 2025

If Something Goes Wrong, How Do I File a Claim?

File a claim on your salon insurance by logging into your BBI account and submitting the claim information under “Manage Policies.” From there, a BBI agent will confirm we’ve received your claim, and a claims adjuster will walk you through the next steps.

Learn more about what to expect: How to File a Claim With BBI.

What Isn’t Covered by Salon Insurance?

Salon insurance is tailored to protect against common claims you face, but it doesn’t cover everything. Here are some examples of things your policy won’t respond to:

- Your own injuries

- Intentional injuries or damage

- Services excluded by the policy

- Independent contractors who work at your salon

- Loss of your tools and supplies (not automatically covered; requires tools and supplies coverage)

- Your business vehicle

- Retail products sold

Read through your policy exclusions to understand exactly what is and isn’t covered.

Employees vs Contractors: Why It Changes Insurance Requirements

Salon owners are liable for the work their hired employees do and any damages they may cause. However, independent contractors are typically responsible for their own work, even though they may offer services in your salon.

It’s crucial to verify who your state considers an employee versus a contractor and carry the proper coverage so you’re protected against liability risks. When the lines are blurred, the responsibility can fall back on you; always ensure employment statuses and liability are clearly defined.

How Much Does Salon Insurance Cost?

BBI’s salon insurance starts from $31.08/month or $349/year, providing invaluable peace of mind to focus on helping clients and managing your business.

Learn more about salon insurance costs to see how affordable coverage can be.

Salon Insurance Costs 101

How much it is: From $31.08/month or $349/year

What affects price: Number of stations and optional coverage add-ons selected

Payment plans: Choose monthly or annual payments

What Affects the Cost of My Policy?

Two factors affect your BBI salon insurance cost:

- The number of stations you want to insure

- Any optional coverage add-ons you select

For example, the monthly premium for a base policy covering three salon stations is $39.42. If you opt for tools and supplies coverage with a $10,000 policy limit, add $5.50/month. In total, your monthly cost is $44.92.

How Do I Avoid Paying for Coverage I Don’t Need?

BBI makes it easy to customize your policy, so you only pay for the coverages you truly need. Select your station tier and optional coverages to create a protection plan that works for you.

Here are some other ways to save.

- Match your tools and supplies coverage limits: Opt for the lowest tier of coverage that protects the value of the business items you actually have

- Confirm contract requirements first: Don’t automatically add additional insureds to your policy unless it’s specifically requested

- Pay annually instead of monthly: You can save up to 6% with one upfront annual payment versus paying monthly

- Consider unlimited additional insureds: If you need to add two or more additional insureds on your policy, choose the unlimited option ($30) instead of paying $15 for each

BBI offers the most affordable, truly salon-level coverage on the market. See why 70,000 beauty and bodywork professionals trust us to protect their businesses with our salon insurance comparison guide.

Protect Your Salon Flawlessly — With BBI

BBI’s coverage is tailored for the salon industry. Our salon insurance is built for the real risks you face and the everyday way you work. Get top-rated coverage that fits your budget so you can focus on what matters most: helping clients look their best.

Protect your salon today!

Have more beauty salon insurance questions? Our friendly, licensed support agents are on standby to help! Contact us.